Advanced Tax Strategies for $400K+ Earners,

Stop Overpaying the IRS

Top Real Estate CPA and Tax Strategists for Investors & Realtors

NOTICE: We receive 25+ real estate consultation requests every week and have only a handful of intake slots left.

Calls are first-come, first-serve.

Top-Rated CPA Firm Serving High-Net-Worth Clients Nationwide

15+

Years of Experience

400+

Clients Served

$50M

Clients Tax Savings

Your CPA Said

"there's nothing more you can do."

This Is What We Actually Did:

International Real Estate Investors recover $95K in tax refunds.

Uncovered missed international deductions and amended prior U.S. filings to recover overpaid taxes.

Applied advanced depreciation strategies across multi-country real estate holdings to maximize benefits.

Recovered $95,000 in refunds—capital reinvested into a new venture supporting expatriates in Mexico.

Real Estate Developers recover $175K in tax refunds.

Conducted a multi-year deep-dive into U.S. tax filings to identify overlooked real estate losses and deductions.

Applied accelerated depreciation strategies and amended prior returns for maximum recovery.

Secured $175K in tax refunds—turning prior setbacks into renewed investment capital.

Doctor saves $400K in taxes using advanced real estate and business tax strategies.

Implemented cost segregation and bonus depreciation to maximize real estate deductions across properties in U.S. and Canada.

Optimized consulting business with entity restructuring, home office, and vehicle deductions.

By the time high earning professionals

find us, they’re frustrated, and rightfully so.

You’re earning at the top of your field.

Yet every year, you watch tens of thousands disappear to taxes.

When you ask your CPA how to fix it, you hear the same answer:

“That’s just part of being successful.”

But deep down, you know that can’t be right.

You are correct.

At Delerme CPA, we fix that.

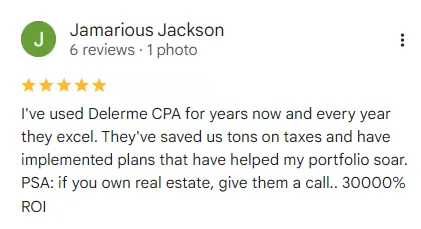

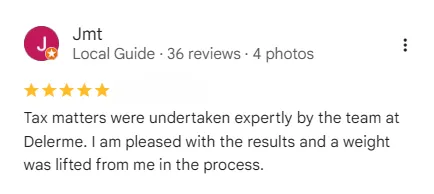

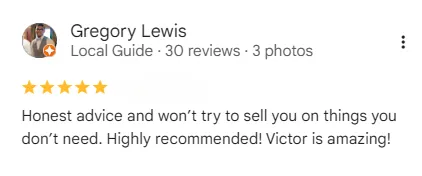

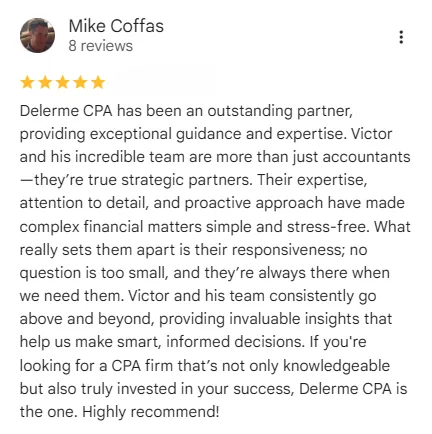

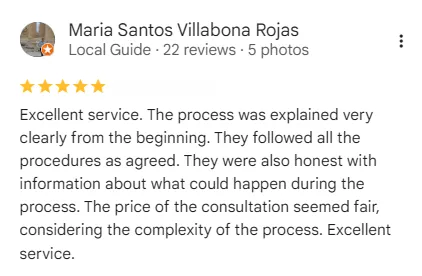

What Our Clients Are Saying

Our clients trust us because we deliver measurable results and lasting peace of mind.

These reviews reflect the real experiences of business owners and high income earners who’ve simplified their finances and maximized their savings with our team.

After our call, you'll walk away with:

A clear picture of why you may be overpaying in taxes.

A personalized projection on how much you can save.

A step-by-step plan to start saving now and prevent future overpayments.

Confidence that your tax strategy is both optimized and compliant.

About Delerme CPA

Wondering why clients choose us?

Because we bring a full tax team to the table—not just one CPA. With in-house tax attorneys, global wealth structuring, efficient communication, and a proven track record with high-income earners, we deliver personalized tax strategies that scale with your success.

In-House Tax Attorneys

Our team includes dedicated tax attorneys who ensure every strategy we implement is 100% legal, fully compliant, and defensible.

For individuals who demand precision and airtight protection, this means your tax savings are built on a rock-solid foundation.

Wealth Structuring

We help structure your finances, from entity structuring, designing advanced retirement plans, and evaluating which investments deliver the greatest tax advantages.

Most high income earners have multiple income streams, we help you leverage them to accelerate long-term wealth.

A Full Tax Team, Not Just One CPA

When you work with us, you’re not limited to a single accountant’s perspective. You get access to CPAs, tax attorneys, enrolled agents, and advisors who bring diverse expertise across industries and jurisdictions.

This team approach means sharper strategies, fewer missed opportunities, and stronger results.

Personalized, Global Solutions

No cookie-cutter strategies here. Every client’s plan is custom-tailored, accounting for cross-border investments, state and federal rules, and evolving financial goals.

With multi-jurisdictional licensing and compliance expertise, we guide you through complex landscapes seamlessly as your needs grow.

Streamlined Access and Communication

You’ll have a dedicated advisor and secure portal to track progress in real time.

Our process is designed for high earners' busy schedules — efficient, transparent, and always available when you need clarity.

Smooth sailing and constant communication are our standards.

Proven Experience for

High Income Earners

With 15+ years of experience and 400+ clients served, our bilingual team specializes in tax planning for high-income individuals and professionals.

We craft strategies tailored to each unique situation, maximizing deductions, reducing taxes, and delivering measurable results most firms can’t match.

A Note from Victor Delerme,

Founder & CPA

"I’ve spent 15 years working exclusively with high-earning professionals, studying exactly where money leaks out—and how to stop it.

This is the same tax strategy system that’s helped hundreds of clients reduce their tax bills by up to six figures, year after year.

Our framework focuses on the few tax strategies that deliver the biggest results, so you don’t waste time chasing scraps or risky loopholes.

We apply what the top 1% already use, proactively and legally."

Frequently Asked Questions

What tax deductions can real-estate investors claim?

Real-estate investors can access a wide array of deductions, but the full picture depends heavily on your specific situation. Here’s how to think about it:

Core Deductions are the most commonly available expenses for rental properties, and investors should generally expect to have many of them:

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Property management fees

- Utilities (when the owner pays)

- Advertising and marketing

- Travel and vehicle expenses for property-related trips (with substantiation)

- Professional fees (legal, accounting, bookkeeping)

- Licenses, permits, HOA or condo fees

- Depreciation (both for the building and allocated components)

- Capital cost allowances—or cost segregation (when applicable)

- Other “ordinary and necessary” business expenses

These deductions are discussed in IRS Publication 527, which covers rental income and allowable expenses.

While the core set covers much ground, many real-estate investors qualify for additional deductions or tax credits (or favorable treatments) depending on their circumstances. These enhancements can meaningfully increase tax savings, which is why it’s critical to tailor the deduction schedule to each client.

What's the difference between a passive investor and a real-estate professional for tax purposes?

Rental activities are generally passive, limiting loss offsets. A taxpayer who qualifies as a real-estate professional (materially participates and meets hourly tests) can treat rental losses as non-passive and offset other income. The rules are technical and fact-specific.

Qualification can unlock against-the-clock offsets for other income.

Do rental profits count as self-employment income subject to SE tax?

Generally, rental income reported on Schedule E is not subject to self-employment tax unless you provide substantial services (e.g., hotel-style services) or hold property as an active business (short-term rentals, dealer activity). Entity structuring can change the analysis.

SE tax can add 15%+ to tax cost if misclassified.

What forms and records should I keep?

Keep leases, closing statements (HUD/ALTA), receipts for repairs/improvements, insurance, bank statements, depreciation schedules, and records of time spent (if aiming for real-estate professional status).

File Schedule E for rentals, Form 8824 for 1031 exchanges, and other entity returns as applicable. Good records protect deductions and simplify audits.

Can I use the Qualified Business Income (QBI) 199A deduction on rental income?

Possibly. Under IRS guidance there’s a safe harbor for rental real estate to qualify as a trade/business for 199A, but you must meet documentation and activity thresholds (e.g., hours and businesslike operations). The rules are complex and require a facts-and-circumstances review.

How do short-term rentals (Airbnb) differ tax-wise from long-term rentals?

Short-term rentals, such as those listed on Airbnb, VRBO, or similar platforms, are treated differently from long-term rentals under IRS rules because the activity may be considered more like a business than a passive investment.

The distinction largely hinges on how much you provide in services and how frequently you rent the property. If you offer substantial services—like daily cleaning, concierge-style amenities, or meal provision—the IRS may classify your rental income as active business income, which could subject it to self-employment tax in addition to regular income tax.

By contrast, long-term rentals (typically leases of 30 days or more without extra services) are usually considered passive income, reported on Schedule E, and not subject to self-employment tax.

Another key difference is the treatment of expenses and deductions. While both long-term and short-term rental owners can generally deduct operating expenses like mortgage interest, repairs, insurance, and property management fees, short-term rental owners may have more flexibility to deduct costs associated with marketing, platform fees, or certain home improvements that cater specifically to guests.

However, because the IRS may consider the property a business, timing and documentation of these deductions become critical. Accurate records of days rented, services provided, and associated costs can make a significant difference if your return is ever reviewed.

Finally, short-term rentals also bring additional state and local tax obligations that long-term rentals might not. Occupancy taxes, business licenses, and local transient lodging taxes are often required for short-term rentals. Plus, the way your income interacts with other business activities—such as eligibility for the Qualified Business Income (QBI) deduction—can be affected by how the IRS classifies your rental. For these reasons, it’s important to carefully review each short-term rental property with a tax professional to ensure compliance and maximize your deductions.

What is a cost-segregation study and should I consider one?

A cost-segregation study reclassifies parts of a building into shorter recovery classes (personal property) so you can accelerate depreciation and increase early-year deductions.

This strategy works best for higher-cost properties or recent purchases/renovations.

You should consider this strategy because bigger early tax shields = better cash flow for growth or debt paydown.

What role should my CPA play in reducing taxes vs. just filing returns?

A high-value CPA (or firm) should not simply be a “tax return filer,” but a proactive tax planner / strategist. Here’s how they differ:

Tax preparer: Backward-looking: collect your documents, fill and file returns. Works mostly around tax season and ensures compliance while claiming deductions you already qualify for.

Tax planner / tax strategist: Forward-looking: design business & financial structure to reduce tax burden. Works all year long, not only during tax season, with periodic reviews. Their strategies lower your future taxes, shift income/deductions optimally, and anticipates changes.

Many CPAs or firms do both roles to a degree, but not all are skilled or experienced in advanced tax planning. Some may stick to preparation because it's lower risk, easier to standardize, or because they lack deep knowledge in strategies for high earners.

Your tax planner should essentially be your partner who sees your full financial picture and integrates planning into your business and personal life.

If these strategies are legal, why hasn't my previous CPA recommended them already?

Just because a strategy is legal doesn’t mean every CPA will (or can) recommend it. Below we'll outline some reasoning behind this:

Scope / specialization: Some CPAs focus primarily on compliance and preparation rather than proactive tax strategy (they may not have training or comfort with riskier structures).

Lack of depth or resources: Advanced planning often involves modeling, projections, multi-jurisdictional work, legal input, and deeper knowledge that not all CPA firms have. Many CPAs operate as a one-person show, which means less expertise among many different sectors and strategies.

Misalignment of incentives: A preparer may not be compensated (or incentivized) to dig into year-round planning.

Client timing / awareness: Many individuals only engage a planner late in the year (or after the tax season) — by then, many strategic “windows” are closed.

At our firm, we blend compliance, planning, and legal oversight (CPAs + tax attorneys) so clients aren’t left relying on one perspective.

How do I evaluate a CPA firm to ensure they're true tax planners and not just tax preparers?

Here’s a quick checklist of traits, questions, and signs of a genuine strategic tax partner:

✔ Credentials & specialization

- Look for CPAs with advanced tax credentials, credentials in multiple jurisdictions (or familiarity with cross-state issues)

- Experience working with high-income professionals (doctors, specialists)

- Partnerships with tax attorneys or in-house legal support

✔ Process and communication

- They should ask forward-looking planning questions (cashflow, risk tolerance, growth plans), not just “give me your W-2s/1099s”

- Year-round check-ins or midyear reviews, not just “once a year”

- Scenario modeling and forecasting, not vanilla “fill in blanks”

✔ Depth of offering

- Offer entity design (LLC, S-Corp elections, professional corp advice)

- Retirement plan design and contribution modeling

- State residency / domicile planning

- Audit defense or proactive documentation support

Your biggest tax savings are waiting, will you claim them or miss out?

DELERME CPA

Copyright ©2026 Delerme CPA. All rights reserved.

Privacy Policy and Terms of Service

LOCATIONS:

Atlanta: 4651 Roswell Road, B105, Atlanta, GA 30342

Puerto Rico: 807 Ave Ponce de Leon PMB 0406, San Juan, PR 00907

Miami: 31 SE 5th Street, Suite CU204. Miami, FL, 33131

CONTACT: 678-585-6580 | [email protected]